Blockchain technology has revolutionized the way we conduct transactions and store data. With its decentralized, immutable, and transparent nature, it has gained widespread adoption in various industries. One of the key features of blockchain is its ability to confirm transactions, ensuring that all parties involved agree on the validity of the transaction. In this article, we will delve into the world of blockchain confirmed transactions, exploring its mechanisms, benefits, and potential use cases.

How Does a Blockchain Confirmed Transaction Work?

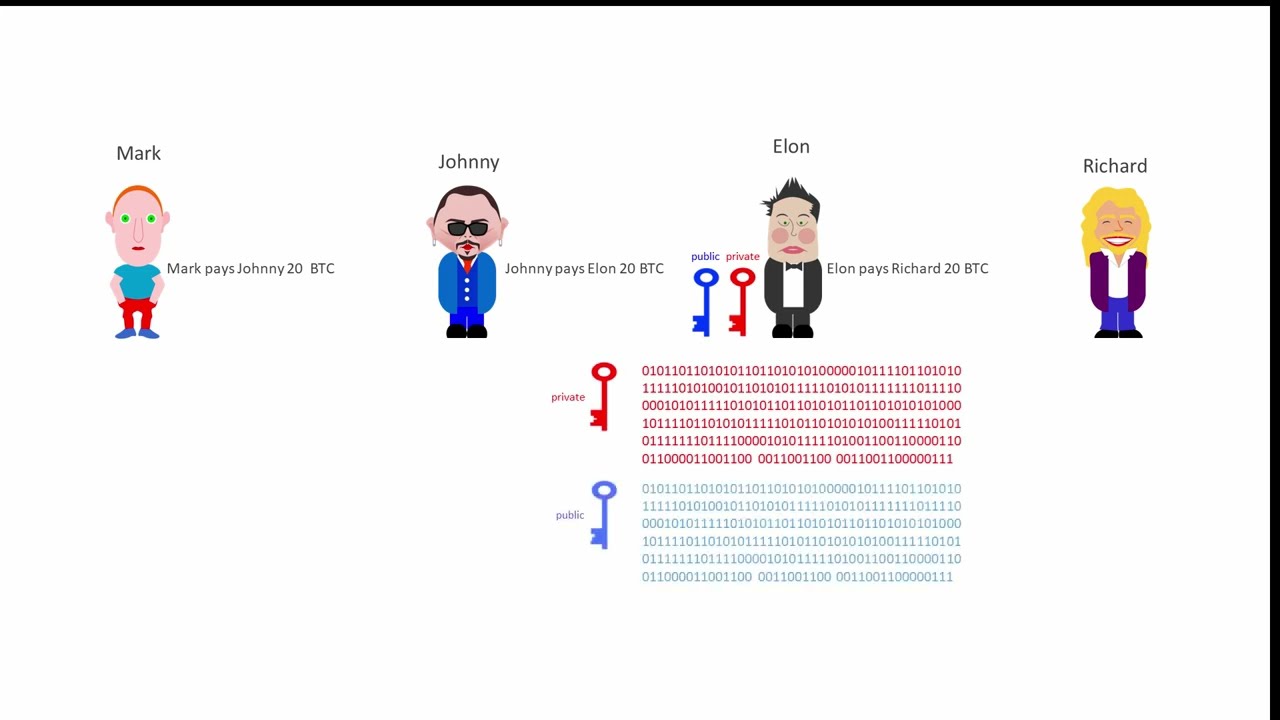

A blockchain confirmed transaction is essentially a record of a transaction that has been validated by the network of computers within a blockchain. When a transaction is initiated, it is broadcasted to the entire network and is then added to a “block” of transactions. This block is then verified and added to the existing chain of blocks, creating a permanent and tamper-proof record of the transaction.

The Role of Miners

Miners play a crucial role in the confirmation of transactions. They are responsible for verifying the validity of each transaction by solving complex mathematical puzzles. Once a miner successfully solves a puzzle, the solved block is added to the blockchain, and the miner is rewarded with a certain amount of cryptocurrency. This process is known as “proof-of-work,” and it ensures the security and integrity of the blockchain.

The Importance of Consensus

Consensus is another integral aspect of blockchain confirmed transactions. In order for a transaction to be confirmed, there must be agreement among the nodes in the network. This consensus mechanism ensures that all parties involved have reached a mutual understanding and have agreed upon the validity of the transaction.

Advantages of Blockchain Confirmed Transactions

The use of blockchain confirmed transactions offers numerous benefits, making it an attractive option for businesses and individuals alike. Some of the key advantages include:

Increased Transparency

One of the main advantages of blockchain technology is its transparency. Since all transactions are recorded on a public ledger, anyone can view and verify them. This level of transparency fosters trust and helps to prevent fraudulent activities.

Improved Security

Blockchain technology employs advanced cryptographic techniques, making it virtually impossible for hackers to manipulate or alter any data on the blockchain. Additionally, the decentralized nature of blockchain ensures that there is no single point of failure, further enhancing its security.

Reduced Transaction Costs

Traditional financial transactions involve intermediaries such as banks and payment processors, leading to added fees and delays. With blockchain technology, there is no need for intermediaries, reducing transaction costs and increasing efficiency.

Increased Efficiency

The use of blockchain technology has the potential to streamline various processes and increase efficiency. Since all parties have access to the same information, there is less room for errors, disputes, or delays.

Potential Use Cases for Blockchain Confirmed Transactions

The applications of blockchain confirmed transactions are endless, as it can be used in various industries and sectors. Some of the most promising use cases include:

Supply Chain Management

Blockchain technology can be leveraged for supply chain management, allowing businesses to track and trace products from their source to the end consumer. This can help to improve transparency, reduce fraud, and enhance the overall efficiency of the supply chain.

Real Estate

Blockchain technology has the potential to revolutionize the real estate industry by making property transactions more efficient and secure. It can also help to reduce the risk of fraud and streamline the process of buying and selling properties.

Healthcare

The healthcare industry is another sector that stands to benefit from blockchain technology. By using blockchain confirmed transactions, patient records can be securely stored and shared between healthcare providers, ensuring accuracy, privacy, and interoperability.

How to Use Blockchain Confirmed Transactions?

There are several ways in which individuals and businesses can utilize blockchain confirmed transactions. These include:

- Sending and receiving payments: Blockchain technology allows for fast and secure peer-to-peer transactions without the need for intermediaries.

- Asset tokenization: By using blockchain technology, physical assets can be digitized and represented as tokens, allowing for easy transfer and ownership tracking.

- Smart contracts: Smart contracts are self-executing agreements that run on the blockchain. They can facilitate a variety of transactions, such as insurance claims or supply chain payments.

Examples of Blockchain Confirmed Transactions

One of the most well-known examples of blockchain confirmed transactions is Bitcoin. Every time a Bitcoin transaction is made, it is confirmed by miners and added to the blockchain, creating an immutable record of ownership.

Another example is VeChain, a blockchain platform that specializes in supply chain management. It uses blockchain technology to track products from their origin to the end consumer, ensuring transparency and authenticity.

Comparing Blockchain Confirmed Transactions with Traditional Transactions

Traditional financial transactions involve multiple intermediaries, making them more complex, expensive, and prone to errors. On the other hand, blockchain confirmed transactions are fast, efficient, and secure, eliminating the need for intermediaries and reducing costs.

Moreover, traditional transactions rely on centralized systems, making them vulnerable to cyber attacks and fraud. In contrast, blockchain technology is decentralized, making it more resilient and tamper-proof.

Advice for Utilizing Blockchain Confirmed Transactions

When utilizing blockchain confirmed transactions, it is essential to consider the following:

- Choose a reputable and established blockchain platform: With the rise in popularity of blockchain technology, numerous platforms have emerged. It is crucial to choose a platform that has a proven track record and a large network of users.

- Be mindful of transaction fees: While blockchain technology can significantly reduce transaction costs, it is essential to keep in mind that some cryptocurrency networks charge fees for confirming transactions.

- Ensure proper security measures: While blockchain technology is inherently secure, it is still susceptible to human error. Therefore, it is crucial to implement proper security measures, such as strong passwords and two-factor authentication, to protect your assets.

FAQs

Q: How long does it take for a blockchain transaction to be confirmed?

A: The time it takes for a transaction to be confirmed varies depending on the blockchain platform and the network’s congestion. On average, it can take anywhere from a few minutes to several hours.

Q: Can blockchain transactions be reversed or cancelled?

A: No, once a transaction has been confirmed and added to the blockchain, it cannot be reversed or cancelled.

Q: Are there any risks associated with using blockchain technology?

A: While blockchain technology offers numerous benefits, there are also some risks involved, such as volatility in cryptocurrency prices and potential security vulnerabilities in the underlying code.

Q: Is blockchain technology only limited to financial transactions?

A: No, blockchain technology can be used for various purposes, including supply chain management, digital identity verification, and healthcare data management.

Q: Do I need to have technical knowledge to use blockchain confirmed transactions?

A: While a basic understanding of blockchain technology may be helpful, most blockchain platforms offer user-friendly interfaces that make it easy for anyone to use without any technical knowledge.

Conclusion

Blockchain confirmed transactions have the potential to revolutionize the way we conduct transactions and exchange information. With its decentralized and transparent nature, it offers numerous benefits and can be utilized in various industries and sectors. As more businesses and individuals adopt this technology, we can expect to see even more innovative use cases and advancements in the world of blockchain confirmed transactions.