Blockchain technology has revolutionized the way we think about transactions. With its decentralized and secure nature, blockchain has become a popular tool for conducting financial transactions, streamlining supply chains, and even voting in elections. But what exactly is a blockchain transaction? How does it work? And what are its benefits and drawbacks? In this comprehensive guide, we will delve into all aspects of blockchain transactions and explore how they are changing the face of traditional transactions.

What is a Blockchain Transaction?

A blockchain transaction is a transfer of digital assets or information using blockchain technology. It is a record of data that is verified, encrypted, and added to a distributed ledger that resides on multiple nodes (computers) in a decentralized network. This makes blockchain transactions secure, transparent, and immutable.

How Does a Blockchain Transaction Work?

In a traditional transaction, a central authority, such as a bank, acts as an intermediary between two parties, verifying and recording the transaction. In contrast, blockchain eliminates the need for a middleman by using a peer-to-peer network to validate and record transactions. Here’s how it works:

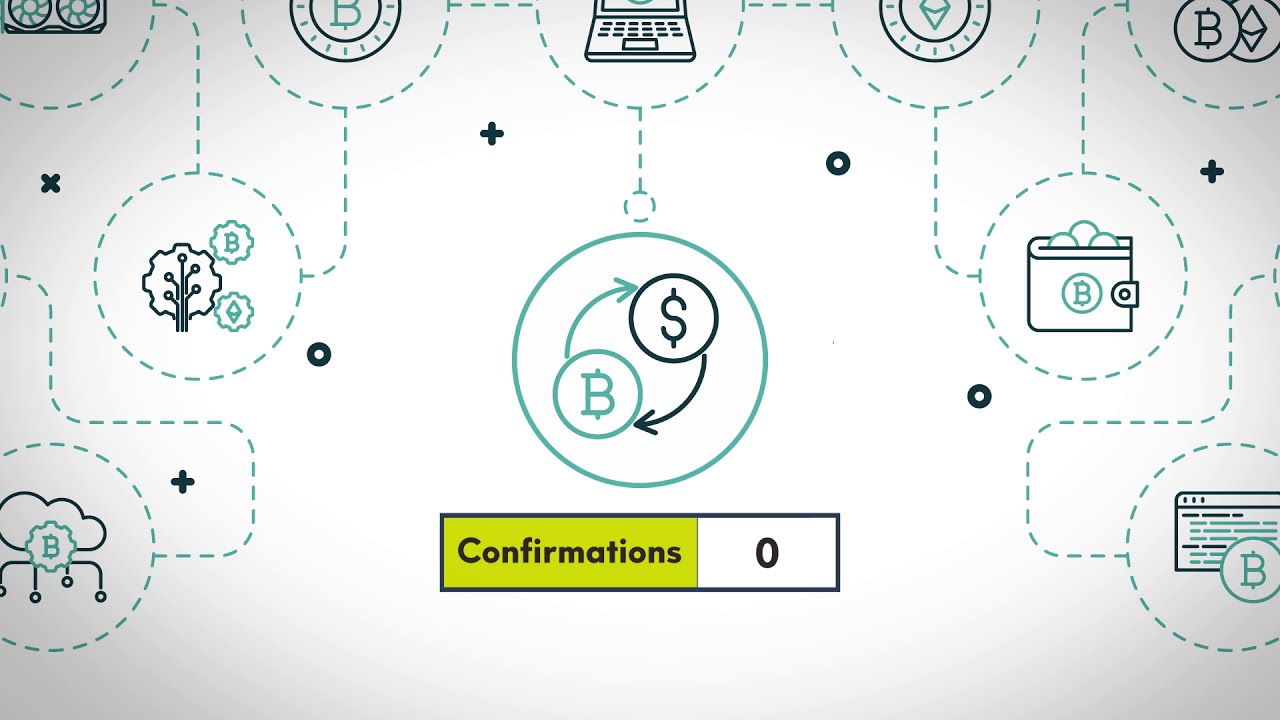

- A user initiates a transaction by sending a request to the network.

- The network nodes verify the transaction by checking the sender’s digital signature and ensuring they have enough funds.

- Once verified, the transaction is bundled with other transactions and added to a new block.

- The block is then added to the existing chain of blocks, creating a permanent record of the transaction.

- The transaction is complete, and both parties can view and track the transaction on the blockchain.

In essence, blockchain technology enables direct and secure transactions without the need for intermediaries, making it faster and more efficient than traditional methods.

Benefits of Using Blockchain for Transactions

Blockchain transactions offer several advantages over traditional methods, including:

- Security: Since transactions are recorded on a decentralized ledger, it is almost impossible to hack or manipulate the data. Additionally, each block in the chain is linked to the previous one, creating a tamper-proof system.

- Transparency: Everyone on the blockchain network can view the transactions, creating a transparent and accountable system.

- Speed and Efficiency: With blockchain, transactions are completed in minutes, eliminating long wait times associated with traditional transactions.

- Lower Fees: Since there are no intermediaries involved, transaction fees are significantly lower compared to traditional methods.

- Global Accessibility: Blockchain technology operates 24/7, making it accessible to anyone with an internet connection, regardless of their location.

- No Intermediaries: By removing intermediaries, blockchain eliminates the potential for third-party manipulation and costly fees.

Drawbacks of Using Blockchain for Transactions

While blockchain offers many benefits, it also has some drawbacks, including:

- Complexity: Blockchain technology is still relatively new and complex, making it challenging for non-technical users to understand and use effectively.

- Limited Scalability: The current blockchain infrastructure can only handle a limited number of transactions per second, making it difficult to scale for mass adoption.

- Regulatory Uncertainty: As a nascent technology, blockchain is not yet regulated, which raises concerns about legal and compliance issues.

- Risk of Fraud: While blockchain is secure, there have been instances of fraudulent coins and scams, highlighting the need for caution when transacting on the blockchain.

Use Cases for Blockchain Transactions

Blockchain transactions have a wide range of use cases, from financial transactions to supply chain management. Here are some examples of how blockchain is being used in various industries:

Financial Transactions

Perhaps the most well-known use case for blockchain transactions is in the financial sector. Large financial institutions, such as banks and credit card companies, have started experimenting with blockchain to streamline and secure transactions. For example, the Santander bank has created a blockchain-based payment system that allows users to transfer money internationally at a fraction of the cost and time compared to traditional methods.

Supply Chain Management

Blockchain is also being used to improve supply chain management. By tracking and recording every step of the supply chain on the blockchain, businesses can enhance transparency and traceability, reducing the risk of fraud and counterfeiting. This technology is particularly useful for industries such as food and pharmaceuticals, where product authenticity and safety are crucial.

Digital Voting

Blockchain technology is also being used to revolutionize the voting process. With its decentralized and secure nature, blockchain eliminates the potential for voter fraud and tampering. In 2018, Sierra Leone became the first country in the world to use blockchain for national elections, and other countries are exploring its use for future elections.

How to Use Blockchain for Transactions

Using blockchain for transactions requires a basic understanding of how the technology works. Here’s an overview of the steps involved in using blockchain for transactions:

- Choose a blockchain platform: There are various blockchain platforms available, each with its unique features and capabilities. Some popular options include Ethereum, Hyperledger, and Stellar.

- Create a digital wallet: A digital wallet is a software program that stores your private keys and enables you to send and receive digital assets.

- Get some cryptocurrency: Most blockchains use their own form of digital currency, which you will need to complete transactions on the network.

- Initiate a transaction: Once you have a digital wallet and cryptocurrency, you can initiate a transaction by sending a request to the blockchain network.

- Confirm the transaction: The network nodes will verify and confirm the transaction before adding it to the blockchain.

- Track the transaction: You can track the status of your transaction on the blockchain using your public key or transaction ID.

Examples of Transactions on the Blockchain

There are numerous examples of transactions on the blockchain, some of which have already been mentioned. Here are a few more examples:

- Cryptocurrency Transactions: Cryptocurrencies are digital assets that can be sent and received using blockchain technology. Bitcoin, Ethereum, and Litecoin are some popular cryptocurrencies that use blockchain for transactions.

- Smart Contracts: Smart contracts are self-executing digital agreements that are programmed to automatically execute when certain conditions are met. They use blockchain technology to store and execute the terms of the contract, eliminating the need for intermediaries.

- Real Estate Transactions: Blockchain is being used to streamline real estate transactions by digitizing and automating the process, reducing paperwork and potential errors.

- Loyalty Programs: Companies can use blockchain to create loyalty programs that allow customers to earn and redeem rewards seamlessly. This eliminates the need for traditional loyalty card systems and simplifies the redemption process.

- Intellectual Property Rights: Blockchain can be used to protect intellectual property rights by creating an immutable record of ownership and copyright.

Comparing Traditional Transactions with Blockchain Transactions

Traditional and blockchain transactions differ in several ways, including:

| Traditional Transactions | Blockchain Transactions |

|---|---|

| Centralized and controlled by a third party | Decentralized and peer-to-peer |

| Require intermediaries to verify and record | No intermediaries needed |

| Can take days or weeks to complete | Completed in minutes |

| Expensive transaction fees | Low or no transaction fees |

| Vulnerable to fraud and tampering | Secure and immutable record of data |

| Limited accessibility | Globally accessible 24/7 |

Despite the benefits of traditional transactions, they are slow, costly, and prone to manipulation, making them less favorable compared to blockchain transactions.

Tips and Advice for Using Blockchain for Transactions

If you’re considering using blockchain for transactions, here are some tips to keep in mind:

- Research different blockchain platforms and choose one that best fits your needs.

- Understand the risks involved, such as price volatility and regulatory uncertainty when dealing with cryptocurrency.

- Familiarize yourself with the technical aspects of blockchain, such as digital wallets and private keys, to ensure the security of your transactions.

- Consider starting with small transactions and gradually increasing as you gain more experience with blockchain technology.

Frequently Asked Questions About Blockchain Transactions

Q: Is it safe to use blockchain for transactions?

A: Generally, yes. Blockchain technology uses advanced encryption and verification methods to secure transactions. However, there have been instances of fraudulent activity and scams, so it’s essential to be cautious and do your research before transacting on the blockchain.

Q: Can blockchain be used for all types of transactions?

A: While blockchain has a wide range of use cases, it may not be suitable for all transactions. For example, certain industries or businesses may still require intermediaries to verify and record transactions.

Q: Are blockchain transactions anonymous?

A: No, blockchain transactions are pseudo-anonymous, meaning that while they do not reveal your identity, they can be traced back to your public key or transaction ID.

Q: Can I cancel a transaction on the blockchain?

A: Once a blockchain transaction is confirmed and added to the ledger, it cannot be canceled or reversed. This is why it’s crucial to double-check all details before initiating a transaction.

Q: How long does it take to complete a blockchain transaction?

A: The time it takes to complete a blockchain transaction depends on the network traffic and the blockchain platform being used. On average, most transactions are completed within minutes.

Conclusion

Blockchain transactions offer a fast, secure, and transparent way to conduct transactions without the need for intermediaries. From financial transactions to supply chain management and even voting, blockchain technology is changing the way we think about traditional transactions. While there are still some challenges to overcome, the potential for blockchain to revolutionize various industries is undeniable. As we continue to see advancements in the technology, we can expect to see even more use cases for blockchain transactions in the future.